EN

EN

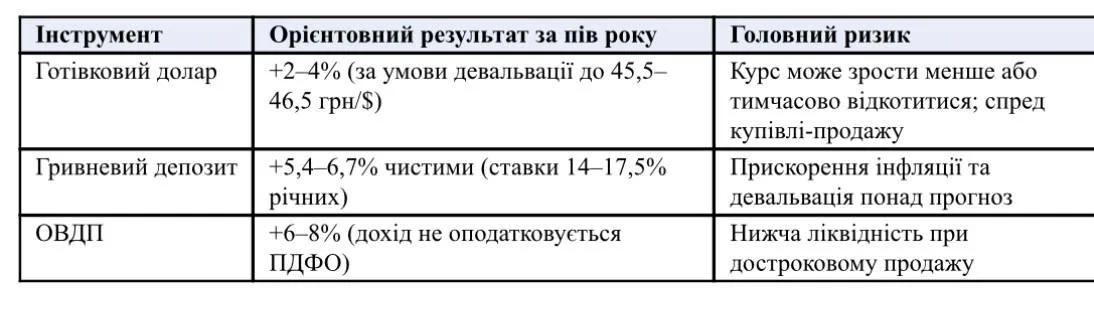

How much can a dollar bring

In July 2026, the official rate will be around UAH 44.6/$, the cash rate will be around UAH 44.5–45.2/$. Most investment companies and bankers expect 45.5–46.5 UAH/$ at the end of the year — a detailed analysis can be found in analysts' forecasts regarding the dollar exchange rate. Even if the upper limit comes true, the growth will be about 2-4% in half a year. That is, someone who buys a dollar today and sells it in December will earn approximately 9-18 thousand hryvnias on 10 thousand dollars — and this is without taking into account the difference between the buying and selling rate, which will eat up part of the result.

The scenario of a sharp devaluation — 47–50 hryvnias/$ — is considered unlikely by bankers: the NBU's international reserves reached a record $51.3 billion in July, and the regulator has plenty to dampen demand spikes. Such a scenario can work only with a simultaneous reduction in foreign aid and a worsening of the security situation.

What hryvnia instruments provide

Banks are currently offering 14–17.5% per annum for hryvnia term deposits. For half a year, this is 7–8.75% "dirty"; after income tax and military levy, about 5.4-6.7% remains. For clarity: a deposit of UAH 100,000 at 14% per annum for six months gives about UAH 5,400 in net income.

Domestic government loan bonds (OVDP) are more interesting than deposits from a tax point of view: their income is not subject to personal income tax, so the rate "on paper" is almost equal to the rate "on hand". Today, you can buy them online through the applications of most large banks and brokers, the entry threshold is from one bond (about a thousand hryvnias).